by Dr Graham Sinden and Jamie Mattison, Ernst & Young

For more than a decade, the debate in Australia around renewable electricity generation has been simmering, alternating between fever pitch and benign interest. The popularity of renewables with consumers is undeniable, with EY research showing that nearly 90 per cent of Australians would consider switching to solar energy. However, electricity utilities face significant current and future market disruption from their increased uptake.

The recent accelerated global rollout of renewable technology has provided an early indication of the ways existing electricity sector operators may be impacted. This growth has been driven by attractive policy settings for renewable energy across a range of locations, including Europe, North America and Australia, together with innovation and investment driving down production costs (by around 80 per cent in five years for solar photovoltaics).

The impacts are starting to be felt not just in network operations, but also in asset valuations.

According to Eurotracker, the five largest power generators in Europe lost over 100billion euros in value from 2008 to 2013, compared to an 18 per cent gain in the German share market over the same period. The scale, and counter-cyclical nature of this change, should be a clear message to operators that the old way of doing business needs to be reevaluated.

Recently, a period of significant policy uncertainty in Australian renewable energy policy was partially addressed, with the government and opposition reaching agreement over a reduction in the legislated Renewable Energy Target (RET); the new target of 33TWh generation in 2020 replaces the original 41TWh. However, there is speculation that this will not altogether end the policy uncertainty that has stalked the renewables market over the past 12 months.

New investment in renewables has fallen around 90 per cent in the 12 months to March 2015 (source: EY, Renewable energy country attractiveness index, June 2015), and a scheduled RET review in 2016 could open the door to further changes and uncertainty.

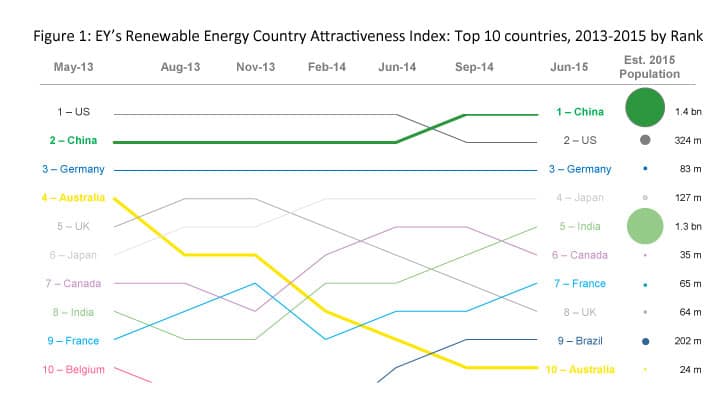

This uncertainty has had a major impact on investor sentiment, and is reflected in EY’s global index that assesses country attractiveness for renewable energy investment and deployment opportunities. Over the period 2013-2015, the period of RET policy uncertainty, Australia has fallen from the fourth most attractive country for renewable energy investment to tenth (out of the 40 countries tracked) – see Figure 1. India and Brazil, along with enthusiastic supporters of renewables in Europe such as Germany and Spain, are now ranked as more attractive investment opportunities than Australia.

Coupled with the size of these markets, and rapid development driving increases in electricity demand in countries such as India (at a time when electricity demand in Australia is falling), further growth in the investment attractiveness of these countries is likely.

However, potential disruption to the sector is not just coming from large-scale renewable projects. Since around 2007, rooftop solar photovoltaics (PV) in Australia have seen significant uptake, initially buoyed by generous feed-in tariffs, but increasingly reflecting the rapid cost reductions seen globally in the solar PV sector, and public sentiment. Australia now has one of the higher levels of solar PV installed capacity globally, with 0.26kW per person installed across the country to date, compared to Germany’s 0.47kW per person in 2014.

The rooftop solar PV sector has been somewhat insulated from the wider policy uncertainty of the RET, particularly once the Government rejected an early recommendation of the 2014 RET Review to bring forward the phasing-out of support for small-scale renewables. The popularity of domestic solar PV may have been a barrier to implementing this recommendation. However, the continuing debate over renewables, likely combined with the scaling back of feed-in tariffs, has seen the year-on-year growth rates for rooftop solar PV slow from a 77 per cent average across 2011 and 2012 to a 25 per cent average across 2013 and 2014 (timing that is consistent with policy uncertainty over the RET).

Figure 1. EY’s renewable energy country attractiveness index: Top 10 Countries, 2013-2015 by rank.

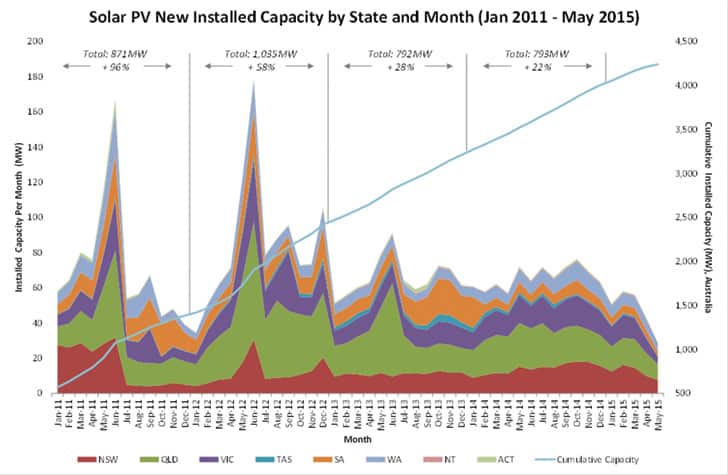

Figure 2. Uptake of rooftop solar PV in Australia.

Yet the domestic solar PV market remains robust: in absolute terms, total installation capacity continues to grow, with 3.7GW added since January 2011 compared to a base of 0.5GW in 2010. And increasingly, it appears that this demand will be driven by fundamental costs. Data published by Deutsche Bank in January showed 39 countries, including Australia, with regions where the long-run cost of electricity from rooftop solar PV costs households less than grid electricity.

What about the grid?

All of this does not mean consumers are taking flight from the grid, or at least not yet.

Solar electricity may be cost-effective, but households use electricity during both day and night. In many regions, grid connection (combined with solar PV) provides a compromise between cost and reliability. But cost reductions in electricity storage could affect this balance, initially in remote or islanded systems where the cost of establishing or maintaining grid connection is high.

The European experience makes it clear that the large-scale rollout of renewable energy projects can have a significant impact on the utilities industry. And while both large and small-scale renewables have played a part in electricity demand falling in Australia, it has been a limited role to-date. Efficiency, demand reduction and price have all played key roles.

Nevertheless, with further declines in solar PV and battery technology costs expected, and as customer knowledge and trust in these products grows, electricity utilities will need to carefully consider how they adapt. Reliable, competitively priced electricity will continue to be a cornerstone of the Australian economy, and the grid and centralised generation will remain key players in delivering these services. However, the sector’s business models, with a need to accommodate innovative finance solutions for renewables or electricity storage, may look significantly different in the future.